Most people focus on profit; it’s the headline number everyone talks about. But profit doesn’t tell you if you can pay your rent tomorrow or your staff next week. Cash flow does. Profit is a snapshot in time; cash flow is your day-to-day reality. It’s the difference between staying in business and just looking good on paper.

🚨The Number 1 Reason Why Businesses Fail

According to ASIC, the number one reason businesses fail is inadequate cash flow or high cash use.

In simple terms, it means not having enough money to cover your expenses when they fall due.

If your sales are strong but the cash isn’t flowing in time, your business can still sink.

Most businesses don’t run out of ideas; they run out of cash. Keep your cash alive, and your business will breathe.

⏱️ This article takes about 9 minutes to read.

What is Cash flow?

Put simply cash flow is the movement of money in and out of your business. You should always maintain a positive cash flow in your business so that you are able to meet your financial obligations. There are many factors that contribute to a positive cash flow and some simple things you can do to keep your business afloat.

There are two main types of cash flow to understand:

1️⃣ Operating Cash Flow:

Money generated from your core business operations and sales.

2️⃣ Financing Cash Flow:

Money from loans or investors, often used for growth, expansion, or purchasing new equipment.

Both are important; one keeps the lights on, the other fuels your next move.

Why Cash Flow Matters

Without consistent cash flow, your business can’t function. Even profitable businesses can collapse if they can’t access liquid funds when needed.

Good cash flow allows you to:

✅ Pay bills and wages on time

✅ Avoid unnecessary borrowing

✅ Plan future growth

✅ Stay attractive to lenders and investors

How to maintain good cash flow

We take a look at some tips and guidelines below on how to maintain a good cash flow for your business.

Create Hidden Bank Accounts

It sounds mysterious, but it’s really just a clever setup within your regular bank account. You can hide money from yourself (in the best way possible) to stay disciplined and plan ahead.

This simple feature changed the way I managed my business finances, and it’s one of the most effective cash flow tools I ever used.

Here’s how it works:

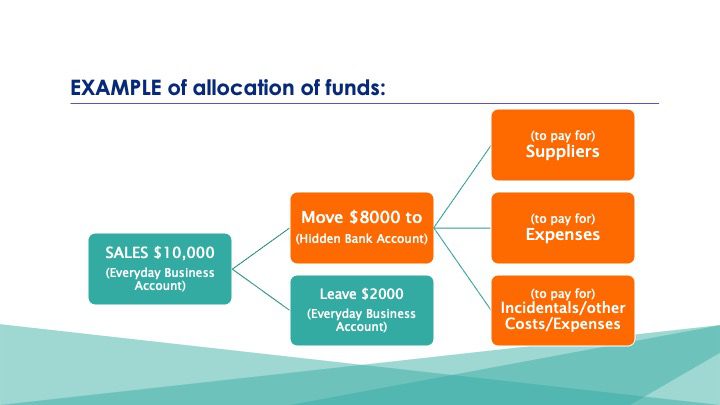

You’ll need two business bank accounts. One’s your everyday account (where all your sales roll in). The other is your hidden account (where you quietly stash away the money that isn’t really yours to spend). You need to manage your revenue.

Let’s say you make $10,000 in sales today, but $8,000 of that will go straight to covering expenses. Move that $8,000 into your hidden account and forget it exists. Now you know your bills are covered, and the $2,000 left in your main account is your real working cash.

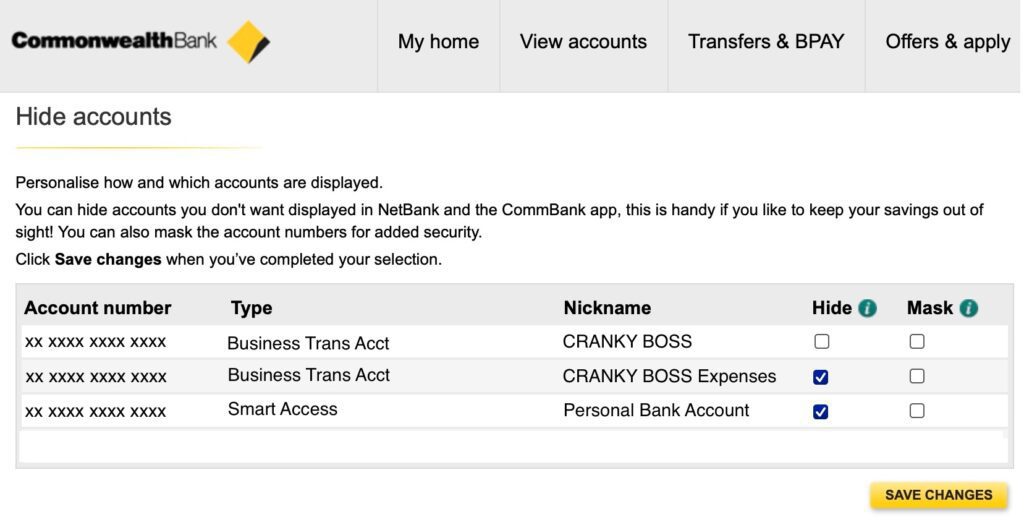

Some banks, such as the Commonwealth Bank, offer a hidden account feature within their online banking platform. When you log in, these accounts do not appear automatically or show in your available funds. You need to click to reveal them, which is what makes them so effective. With a simple click, you can choose to hide or unhide them whenever you like.

If your bank does not have this feature, you can open a second business account with another bank. It will work the same way by giving you a separate place to move your funds where they are out of sight and out of mind.

(See below snapshot of Commonwealth Bank feature that allows you to hide bank accounts:)

My hidden bank accounts became the most powerful tool I had for managing cash flow and avoiding financial stress. The money in those accounts was off limits, and I treated it that way. Over time, I trained myself to forget they even existed. Out of sight, out of mind.

Automate Regular Transfers

Set up automatic weekly or monthly transfers into your “hidden” or “tax” accounts.

Automation removes emotion; you don’t have to rely on willpower to do the right thing.

It’s the easiest discipline you’ll ever build.

Track Your Cash Flow Weekly

Cash flow isn’t something to check once a quarter; make it part of your weekly routine.

Every Friday, take ten minutes to look at:

- What came in this week

- What’s due next week

- Any upcoming bills or renewals

This habit keeps you proactive instead of reactive.

A simple spreadsheet or accounting dashboard (Xero, MYOB, or QuickBooks) is enough to spot early warning signs.

Separate GST, Tax & Super Accounts

Many business owners get caught out at tax time because those funds were never set aside. Open separate sub accounts and transfer a percentage of every sale:

- 10% GST (if applicable)

- 15–25% for income tax

- Super contributions (if employing staff)

It’s not extra admin, it’s peace of mind. When the tax office calls, you’re already covered.

Starting a Business

New in Business? Have a business plan. Get a realistic view on what your start-up costs are and then add some more.

💬 I had a customer who spent 250K opening a brick-and-mortar store and had no funds to buy product! That’s like starting a bakery without flour. That’s not a great way to start a supplier-buyer business relationship.

Budget carefully for:

- Product or inventory

- Marketing and promotion

- Licensing and insurances

- Emergency reserves

Start small, stay flexible, and remember: you don’t need to spend big to look successful. In fact there are some affordable strategies for small businesses that you may not have thought of.

Operating Expenses

You should ideally be able to cover at the very least 3 to 6 months of operating expenses at any given time. (Operating expenses are generally things like rent, wages, utility bills – all those things you need to pay for every month, to keep your business running)

This buffer will protect your business from shocks, whether it’s a quiet sales month or an unexpected bill.

Profitability

Don’t expect profit from day one. Most businesses take 1–4 years to become consistently profitable.

Plan for a slow start, focus on building solid customer relationships, and manage expectations early.

Business Growth

Grow gradually and responsibly.

Early on, you’ll wear multiple hats: marketing, sales, customer service, and admin.

Hold off on hiring or upgrading premises until your revenue supports it.

You will need to initially put in a lot of time and effort to make your business work. Don’t rush to hire employees as tempting as it may be. Do as much as you can yourself. You will have to work ON and IN the business initially. Wait for your business to grow before going and renting a bigger or newer premises.

Control Inventory

Stock ties up cash. Order smart, not big.

Use sales data to understand what actually sells, and reorder based on trends instead of guesses.

If something’s been sitting on a shelf for six months, turn it back into cash; discount it or bundle it.

Look at adopting strategies such as the JIT production strategy.

When I built up stock, I stuck with the best sellers. No experiments, no risks I didn’t need. I never carried more than 50 percent of what I sold the year before. It kept my risk low and my cash available; a simple rule that became part of my risk management playbook.

Forecast Seasonality

Every business has ups and downs. Use past data to predict slow months, and save during the good ones.

Retailers, for instance, should stockpile cash during busy seasons to cover quieter periods. Think of it as your business winter fund.

Business Spending

Spend no more than you can afford. Forget about that bleisure trip that you’re claiming as a business expense. There’s no point claiming it as an expense, if you simply can’t afford it. Give that money to your accountant; its better spent and it’s still an expense!

I will show you a free way to travel and it can be business or first class!

Business Expenses

Trim the fat. There’s always something to cut. Keep reviewing your:

- Subscriptions and memberships

- Utilities and insurance

- Supplier pricing and contracts

A quarterly review of your expenses can instantly improve your cash flow.

Negotiate Better Payment Terms with Suppliers

Cash flow isn’t just about what comes in, it’s about what goes out.

Talk to your suppliers and see if you can stretch payment terms slightly, especially once you’ve built trust. Even moving from 14 day to 30 day terms can make a big difference to your working capital.

Debtors & Credit

Try to avoid offering credit to your customers whenever possible. If you must, keep the payment period short or negotiate stricter terms. For example, instead of giving 30 days of credit, set both a time limit and a dollar limit; whichever comes first. This way, if a customer reaches their credit limit in seven days, you can collect your money sooner instead of waiting until the end of the month.

Invoicing

You don’t get paid if you don’t invoice!

Many small business owners lose cash flow simply because they delay invoicing.

Automate this with software like Xero, MYOB, or QuickBooks.

Cash Flow Assistance

If you need cash flow assistance talk to your bank about which line of credit may assist you. In my experience a bank overdraft was the best option in terms of flexibility and rates. Keep away from credit cards for cash flow issues as their interest rates are very high and this could land you in even bigger trouble. Stay away from high interest lenders.

Cash Flow Forecast

A cash flow forecast helps you see what money is coming in and what money is going out at any time. It’s a simple way to stay prepared. Record how often your expenses occur and put money aside in advance.

For example, if your WorkSafe bill is $12,000 a year, set aside $1,000 each month. Now imagine you have three more annual bills like that. That’s $36,000 that could hit you all at once if you’re not ready. For a small business, that kind of surprise could be a serious setback, or even wipe you out completely.

⚠️ Cash Flow Problems Can Create:

🚫 Unpaid staff wages and super

🚫 Bad credit ratings

🚫 Supply chain issues and blacklisting

🚫 Damaged reputation and trust

🚫 Inability to purchase stock or inventory from suppliers

Avoiding these starts with simple daily discipline and awareness of where your money is going.

Watch for Early Warning Signs

If your overdraft keeps increasing or your payables list is growing faster than receivables, don’t ignore it. Cash flow issues rarely fix themselves.

Act early: adjust spending, renegotiate terms, or tighten credit before it spirals.

🔑 Key Takeaways

💡 Cash flow is the lifeblood of your business; manage it, protect it, and forecast it.

💡 Hidden bank accounts and consistent forecasting can save you from sudden shocks.

💡 Plan for growth responsibly; profit takes time.

💡 Stay disciplined, stay realistic, and always keep sight of your numbers.

Final Words

Profit is important. It shows long term success, but cash flow is survival.

You can have profit on paper and still run out of money because your bills are due before your income arrives.

It’s cash flow that keeps the lights on, the wages paid, and your business moving forward.

Think of profit as your scoreboard, but cash flow as your heartbeat.

One tells you how well you’ve played; the other keeps you alive to play again tomorrow.

When you manage your cash flow well, profit will eventually follow, but it never works the other way around.

Inadequate Cash Flow or High Cash Use is the number one (out of the top four) reasons why businesses fail.

Let’s check out the other reasons why businesses fail & see more information on each:

It’s essential to understand these four reasons as they have critical information to the success of your Finances and Strategic Management which is one of the most important steps in the 5 basic step guide to running a successful business.

✍️ About The Author

From building a thriving company to mastering the frequent flyer game, Cranky Boss has learned that in both business and travel, the journey teaches more than the destination. A Melbourne Business Awards finalist with a knack for building strong teams and keeping things real, Cranky Boss shares the wins, the mishaps, and the occasional “OMG” moments along the way.

Today, Cranky Boss brings real stories, sharp insights, and a grounded perspective from the boardroom to the boarding gate.

Read more about Cranky Boss →

✍️ Quick Facts

Miles flown: Closing in on one million | Hidden talent: Turning frequent flyer points into first class tickets | Coffee strength: Dangerously high | Office pet peeve: Speakerphone calls | Business mantra: Culture first, profit follows | Superpower: Understanding people before they speak.